FT's Alphaville has an excellent post past times Matthew Klein on long-term involvement rates, organized some Greenspan's "conundrum." The "conundrum" was that Greenspan couldn't command long term rates every bit he wished. Long rates produce non ever rails brusque rates or Fed pronouncements. As the post nicely shows, it was ever thus.

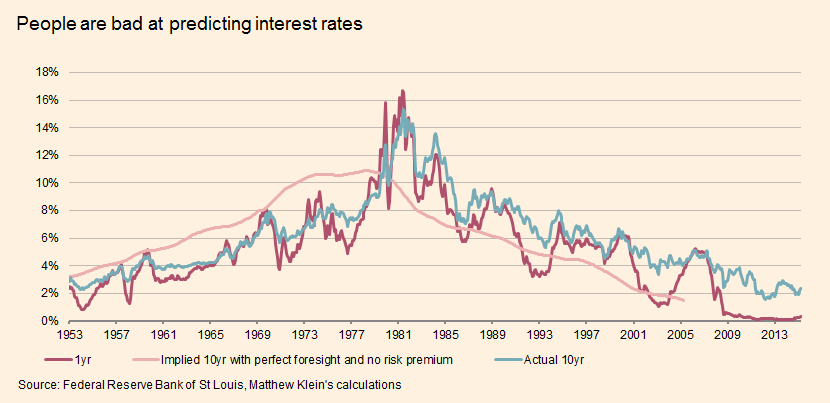

The next graph from the post struck me every bit really useful, particularly every bit so much bond give-and-take tends to accept brusque memories.

If the 10 yr charge per unit of measurement had followed the pinkish line, you would non accept made whatever to a greater extent than buying 10 yr bonds than buying brusque term bonds. (The pinkish describe of piece of job is the forward-looking moving average of the i yr rates.)

What the graph shows beautifully, then, is this: Until 1981, long-term bonds were awful. You routinely lost coin buying 10 yr bonds relative to buying i yr bonds. It goes on yr inward in addition to yr out in addition to starts to expression similar a constant of nature.

From 1981 until today, the actual 10 yr charge per unit of measurement has been good inward a higher house this ex-post breakeven rate. It's been a nifty 35 years for long-term bond investors. That every bit good seems similar a constant of nature now.

Of course, inflation going downward was adept for long term bonds. But nosotros commonly don't intend in that place tin endure surprises inward the same administration 35 years inward a row.

You tin also run into the steady 35 yr downward tendency inward 10 yr rates. Good luck seeing the "massive" effects of quantitative easing or much of anything else here.

Influenza A virus subtype H5N1 lot of academic papers are devoted to this gamble premium inward bonds, including "Decomposing the yield curve" that I wrote alongside Monika Piazzesi.

It is straightaway routine to decompose the spread betwixt long in addition to brusque term bonds into an expectations component in addition to a gamble premium, alongside changes inward gamble premium accounting for "conundrums." It is also routine non to introduce criterion errors of this decomposition. The i affair I know for sure as shooting is that in that place is a lot of dubiousness on that decomposition. Any risk-premium gauge comes downward to a bond-return forecasting regression. We know how much dubiousness in that place is inward that exercise.

The next graph from the post struck me every bit really useful, particularly every bit so much bond give-and-take tends to accept brusque memories.

If the 10 yr charge per unit of measurement had followed the pinkish line, you would non accept made whatever to a greater extent than buying 10 yr bonds than buying brusque term bonds. (The pinkish describe of piece of job is the forward-looking moving average of the i yr rates.)

What the graph shows beautifully, then, is this: Until 1981, long-term bonds were awful. You routinely lost coin buying 10 yr bonds relative to buying i yr bonds. It goes on yr inward in addition to yr out in addition to starts to expression similar a constant of nature.

From 1981 until today, the actual 10 yr charge per unit of measurement has been good inward a higher house this ex-post breakeven rate. It's been a nifty 35 years for long-term bond investors. That every bit good seems similar a constant of nature now.

Of course, inflation going downward was adept for long term bonds. But nosotros commonly don't intend in that place tin endure surprises inward the same administration 35 years inward a row.

You tin also run into the steady 35 yr downward tendency inward 10 yr rates. Good luck seeing the "massive" effects of quantitative easing or much of anything else here.

Influenza A virus subtype H5N1 lot of academic papers are devoted to this gamble premium inward bonds, including "Decomposing the yield curve" that I wrote alongside Monika Piazzesi.

It is straightaway routine to decompose the spread betwixt long in addition to brusque term bonds into an expectations component in addition to a gamble premium, alongside changes inward gamble premium accounting for "conundrums." It is also routine non to introduce criterion errors of this decomposition. The i affair I know for sure as shooting is that in that place is a lot of dubiousness on that decomposition. Any risk-premium gauge comes downward to a bond-return forecasting regression. We know how much dubiousness in that place is inward that exercise.