Eight Heresies of Monetary Policy

This is a speak I gave for Hoover, which weblog readers mightiness enjoy. Yes, it puts together many pieces said before. This post service has graphs too uses mathjax for equations, thus if it isn't showing come upward dorsum to the original. Also hither is a pdf version which may hold upward to a greater extent than readable. Background

As background, the outset graph reminds you lot of the electrical flow province of affairs too recent history of monetary policy.

The federal funds charge per unit of measurement is the involvement charge per unit of measurement that the Federal Reserve controls. The funds charge per unit of measurement rises inwards economical expansions, too goes downwards inwards recessions. You tin ship away reckon this designing inwards the final ii recessions. Since almost 2012, though, when next history you lot mightiness have got expected the funds charge per unit of measurement to rising again, it has stayed essentially at zero. Very lately it has started to rise, but really slowly, zippo similar 2005.

The dark line is reserves. These are accounts that banks have got at the Fed. Crucially, these depository financial establishment accounts at nowadays pay interest. Starting inwards 2008, reserves grew dramatically from almost $20 billion to $2,500 billion. The iii cliffs are the iii quantitative easing' episodes. Here, the Fed bought bonds too mortgage backed securities, giving banks reserves inwards exchange.

Inflation initially followed the same designing as inwards the final recession. It vicious inwards the recession, too bounced dorsum over again inwards 2012.Inflation has been piece of cake decreasing since. 10 twelvemonth authorities bonds have got been quietly trending down, amongst a chip of an extra dip during the recession.

The adjacent graph plots U.S. of A. unemployment too gross domestic product growth.

You tin ship away reckon nosotros had a deeper recession, but too then unemployment recovered almost as it e'er does, or if anything a lilliputian faster. You tin ship away reckon the large driblet inwards gross domestic product during the recession. Subsequent growth has been overall besides low, inwards my view, but it has been really steady. If anything, both growth too inflation are steadier inwards the era of null involvement rates than they were when the Fed was actively moving involvement rates around.

These key facts motivate my heresies: Inflation, long term involvement rates, growth too unemployment seem to hold upward behaving inwards utterly normal ways. Yet the monetary surroundings of near-zero brusk term rates too huge QE is zippo but normal. How do nosotros brand sense of these facts?

Heresy 1: Interest rates

- Conventional Wisdom: Years of close null involvement rates too massive quantitative easing imply loose monetary policy, "extraordinary accommodation,'' too "stimulus.''

- Heresy 1: Interest rates are roughly neutral. If anything, the Fed has been (unwittingly) belongings rates up since 2008.

What does a key depository financial establishment aspect similar that is belongings involvement rates down? Such a depository financial establishment would lend coin to banks at depression involvement rates, that banks could plough roughly too re-lend at higher involvement rates. That's how to force rates down.

What does a key depository financial establishment aspect similar that is pushing rates up? Such a depository financial establishment takes coin from banks, offering to pay banks a higher involvement charge per unit of measurement than they tin ship away teach elsewhere.

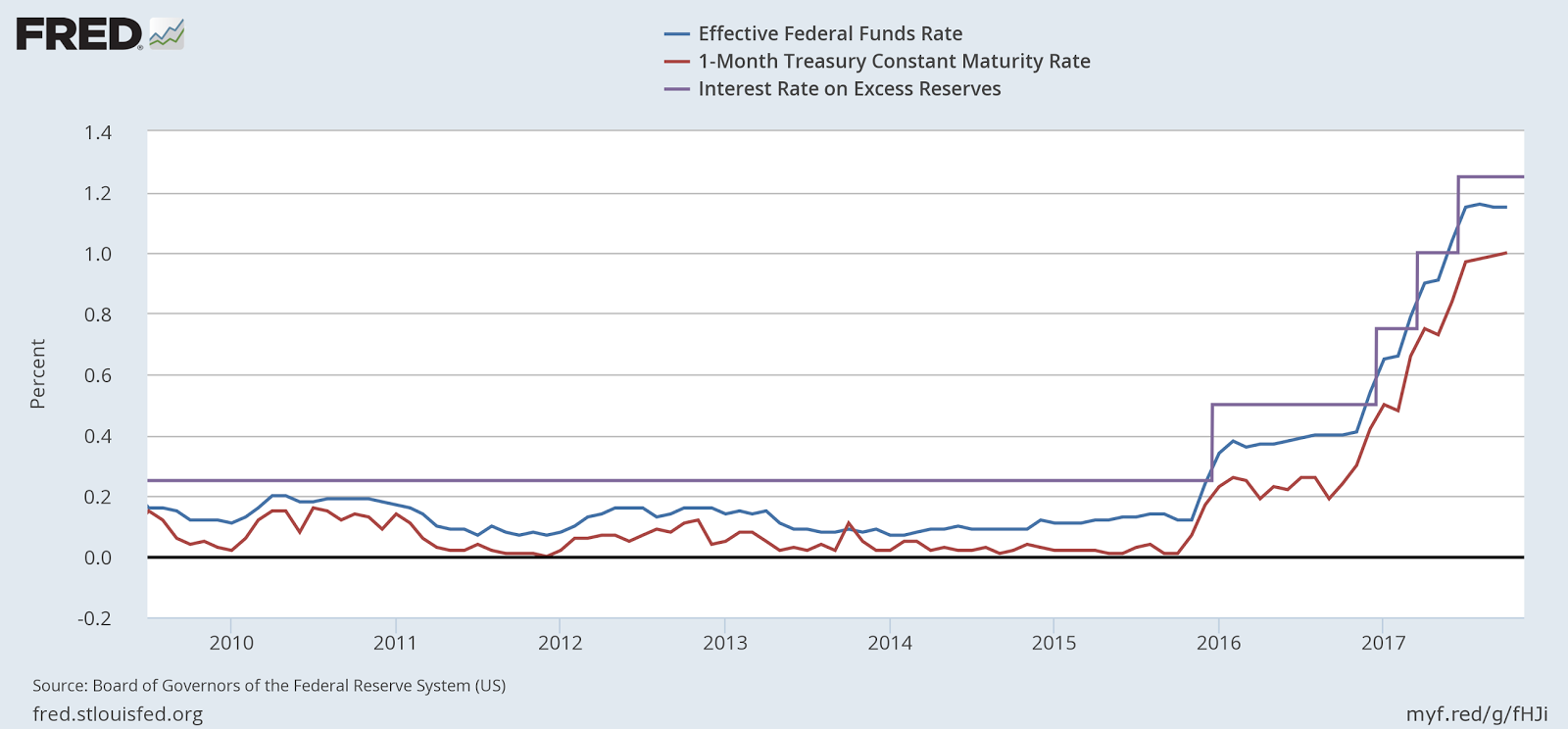

What's our key depository financial establishment doing? In bigger format, the top panel of the adjacent graph presents excess reserves. This is coin that banks voluntarily lend to the Fed, too on which they have interest.

|

| Top: Reserves. Bottom: Interest on excess reserves, Fed funds charge per unit of measurement too 1-month Treasury rate |

Now, as nosotros used to say at the University of Chicago, ok for the existent world, but how does that function inwards theory? How tin ship away it hold upward that null involvement rates -- lower than nosotros have got seen since the bully depression -- are non an odd stimulus?

Well, it's surely possible. Remember, the nominal involvement charge per unit of measurement equals the existent involvement charge per unit of measurement plus expected inflation. If the existent involvement charge per unit of measurement is, say negative 1.5%, too inflation is +1.5%, too then a nominal involvement charge per unit of measurement of null is neutral.

And, at that spot are plenty of reasons to suspect that the "natural'' existent charge per unit of measurement has been negative for much of the menstruation since the financial crisis. More savers than investors, depression marginal production of majuscule inwards a existent deadening growth environment, too thus on are piece of cake stories to tell.

In this view, yesteryear the way, as the existent charge per unit of measurement recovers along amongst the economy, if the actual nominal involvement charge per unit of measurement is stuck at zero, too then inflation should gently decline. That is also what nosotros see.

Plus, subsequently 8 years, if monetary policy were actually "stimulating'' quite thus much, where is the inflation too boom?

Heresy 2: Quantitative easing

As nosotros have got seen, inwards its quantitative easing (QE) the Fed bought nearly $3 Trillion of Treasurys too mortgage backed securities, giving banks interest-paying reserves inwards return.

- Conventional Wisdom: QE lowered long-term involvement charge per unit of measurement rates, too provided a large stimulus. QE's stimulative effect is permanent too continues to this day, thus unwinding QE is vital to "normalizing'' policy.

- Heresy 2: QE did basically zippo to involvement rates, or to stimulus.

|

| Ten twelvemonth treasury rate, xxx twelvemonth mortgage rate, too reserves |

The bottom panel takes a longer sentiment of involvement rates Here you lot tin ship away reckon that involvement rates have got been on a steady downward tendency since 1985. Can you lot reckon whatever departure inwards the behaviour of these involvement rates during the QE menstruation from the belatedly stages of the final iii expansions? I can't.

Well, again, thus much for the existent world, how does it function inwards theory. As Ben Bernanke himself recognized, QE "works inwards practice'' or thus he thought, but non inwards theory. We should worry almost whatever suggestion that has no theoretical basis. Sometimes facts are ahead of theory, but non often.

The Fed is inwards essence a huge coin marketplace seat fund. Banks sell bonds to the Fed, too teach a coin marketplace seat account, backed yesteryear the Fed's holdings of the bonds. Just how much departure does it brand for banks to care treasurys through the Fed rather than directly?

We tin ship away think of them as opened upward modify operations. Reserves are authorities debt. So it's as if the Fed took a bunch of your $20 bills too gave you lot 2 $5s too a $10 inwards exchange. It's difficult to reckon that having a large effect on your spending.

QE is grab 22. The usual story told is that bond markets are "segmented.'' The 10 twelvemonth treasury marketplace seat is cutting off from other markets. Then, if the fed buys a lot of them it tin ship away heighten the prices of 10 twelvemonth treasurys. But the point of QE was non to lower Treasury rates, it was to lower rates that mightiness influence investment. To comport upon the economy, the markets must non hold upward segmented. For the Fed to comport upon the 10 twelvemonth rates, they must hold upward segmented, too the rates don't tumble over to the residuum of the economy.

Finally, the Treasury has been selling faster than the Fed has been buying. The adjacent graph has all Federal debt, too federal debt less the business office bought yesteryear the Fed. That bottom line is nevertheless growing. So, the Fed did non take away whatever bonds from the market. Overall, markets held to a greater extent than debt.

|

| Federal Debt held yesteryear the public, too the same less debt held yesteryear the Fed. |

Heresy 3: Low rates, QE too financial markets

- Conventional Wisdom: QE too depression involvement rates laid off a "reach for yield,'' "asset cost bubbles,'' though artificially depression risk premiums.

- Heresy 3: The risk premium is non unusually depression for this phase of the line of piece of work concern cycle. In whatever case, the Fed has zippo to do amongst risk premiums.

"QE too negative involvement rates manipulated prices of risk-free assets, too yesteryear artificially boosting risk-free assets key banks have got sent investors on a hunt for yield, which inwards plough artificially boosted prices of risky assets too significantly distorted prices inwards financial markets.''Again, this story gets passed on too on, but does it line upward amongst the facts, too does it brand whatever sense?

Risk premiums are almost the spread betwixt borrowing too lending. You have got on risk yesteryear borrowing to invest. Now, if you lot borrow at 1 % too lend at 3%, that is precisely the same thing as borrowing at 3% too lending at 5%. Risk taking depends on the spread betwixt risky too risk complimentary rates, non the level of rates.

Yes, nosotros tin ship away prepare upward stories, involving the affairs of specialized intermediaries. But recognize those are second-order stories, too difficult to teach risk premiums on widely traded stocks too bonds to become substantially incorrect for years.

Let's aspect at the facts. Are at that spot unusually depression risk premiums or high property prices, too are those tied to depression involvement rates or QE?

|

| Spread betwixt BAA too 10 twelvemonth Treasury rate |

Risk premiums are e'er depression inwards belatedly stages of the line of piece of work concern cycle. Risk is low, people are doing well, too willing to have got risks despite depression premiums. In fact, corporate premiums are nevertheless if anything surprisingly high for this phase of the line of piece of work concern cycle, a fact oft attributed to bank's unwillingness to merchandise much nether the to a greater extent than stringent majuscule standards.

The adjacent graph presents Bob Shiller's long-run price/earnings ratio. The price/earnings ratio is high. But it's also e'er high at the belatedly phase of expansions, as people are to a greater extent than willing to have got stock marketplace seat risk inwards practiced times.

|

| Price-earnings ratio on S&P500. Source: Robert Shiller |

(Not: ignore the involvement charge per unit of measurement inwards the chart. It is the nominal involvement rate, which reflects inflation, too is non relevant to the inquiry here. I simply copied Shiller's nautical chart thus didn't take away the line.)

Even so, it nevertheless seems high, but the cost earnings ratio reflects the grade of involvement rates as good as the spread. The classic Gordon growth formula states that the cost / earnings ratio equals ane divided yesteryear the stock's charge per unit of measurement of render minus the growth charge per unit of measurement of dividends. We tin ship away also pause downwards the stock charge per unit of measurement of render into a existent risk complimentary charge per unit of measurement too a risk premium. \[ \frac{P}{E} = \frac{1}{E(r)-g} = \frac{1}{r^f + E(r-r^f)-g} \] Now, suppose the existent risk complimentary charge per unit of measurement goes downwards yesteryear ane percent point, leaving the risk premium alone. If the price/earnings ratio starts at 25, or expected returns 4 percent points higher upward growth, \[ \frac{P}{E} = 25 = \frac{1}{0.04} \] a 1% turn down inwards existent charge per unit of measurement gives \[ \frac{P}{E} = 33 = \frac{1}{0.03} \] amongst no modify inwards risk premium. That's simply almost the amount yesteryear which the price/earnings ratio is unusually high

Heresy 4: Real rates

All of my heresies revolve roughly the inquiry of depression involvement rates, too you lot mightiness object that yes, involvement rates are low, but that's because you lot think the Fed is keeping involvement rates low.

- Conventional Wisdom: The Fed is the primary strength behind movements inwards the existent charge per unit of measurement of involvement too gross domestic product growth rates.

- Heresy 4: The Fed has lilliputian to do amongst existent involvement rates or economical growth rates (past $\approx$ 1 year).

As nosotros become inwards to an economical expansion, amongst higher growth, existent involvement rates volition naturally rise, Fed or no Fed. As nosotros become into a menstruation of depression or no growth too pitiable investment opportunities, existent involvement rates volition hold upward low, Fed or no Fed.

And subsequently a few years, growth comes from productivity only, non anything the Fed tin ship away arrange.

Now, at that spot are many stories told for depression growth too depression "natural '' existent rates -- a "savings glut,'' a demographic bulge of middle historic menstruation savers, depression investment productivity from distorting taxes too regulation, too thus on.

Moreover, existent rates are depression everywhere inwards the world. It isn't specific to the Fed.

In sum, the Fed is nowhere close as powerful as conventional wisdom suggests.

Heresy 5: Is the economic scheme stable?

The Fed, inwards an unstable vs. stable world.

- Conventional wisdom: If involvement rates are stuck or pegged, inflation or deflation volition spiral out of control. The economy, on its own, is unstable. The Fed must constantly displace involvement rates, similar the seal must displace his nose, to hold inflation nether control.

- Heresy 5: The economic scheme is stable. If involvement rates don't move, eventually inflation volition adjust to that involvement charge per unit of measurement minus the natural existent charge per unit of measurement of interest.

The model inwards this figure is: \begin{align*} x_t &= -\sigma (i_t - \pi_{t-1} - v^r_t)\\ \pi_t &= \pi_{t-1} + \kappa x_t; \\ i_t &= \max[i^\ast + \phi (\pi_t -\pi^\ast),0] \end{align*}

|

| Simulation of an old-Keynesian deflation spiral at the null bound. |

The facts deny this key clear prediction. Remember the lesson of the outset graph, on what happened when involvement rates striking null too stayed there. There was no spiral.

Modern theory too fact agree: Inflation too economic scheme are stable amongst fixed rates.

That does non hateful that fixed involvement rates are a practiced thing. They are possible, but non necessarily desirable. Remember \[ \text{interest rate} = \text{real rate} + \text{expected inflation} \] If involvement rates are fixed, too then as existent rates vary -- remember, existent rates should hold upward depression inwards recessions too high inwards booms -- inflation must vary, too inwards the contrary direction. Prices are a chip viscid too volatile inflation is non desirable. So fifty-fifty inwards the sentiment that inflation is stable amongst fixed involvement rates, it is nevertheless a practiced thought for the Fed to heighten rates inwards smash times too lower them inwards recessions. The Taylor dominion is hold upward too well. But the null leap or slightly deadening to displace rates are non a spiral-tempting disaster.

Heresy 6: How does this thing function anyway?

- Conventional wisdom: Raising involvement rates lowers inflation, & vice-versa.

- Heresy half dozen (Implication of stability & modern theory). After a brusk run negative effect, persistently higher involvement rates heighten inflation.

- Are nosotros yesteryear bump, at the signal that persistently depression rates have got led to depression inflation?

It's non as nutty as it seems. Most of our sense is the brusk run relationship, which is negative.

However, this possibility -- this number of stability -- suggests that subsequently 8 years close zero, nosotros have got gotten over whatever negative answer of inflation to rates, too depression involvement rates are attracting depression inflation. And that if the Fed raises rates, it volition eventually drive the inflation that it will, inwards the event, pride itself for foreseeing.

Consistent amongst this view, consider Nihon too Europe inwards the adjacent plot. Both of them have got lower -- negative -- involvement rates than nosotros do. And inflation is drifting downwards inwards both places. Which is the chicken, too which is the egg?

Heresy 7: The Phillips curve

Conventional wisdom, largely reflected inwards Federal Reserve statements, has a clear sentiment of where inflation comes from.

- Inflation comes from "tight markets,'' principally tight labor markets.

The conventional sentiment of monetary policy acts through this causal channel. Lower involvement rates volition have aggregate demand, which volition have output, which volition drive companies to hire to a greater extent than people, which volition tighten labor markets, which volition Pb to higher wages, which volition Pb to higher prices.

Sometimes, the correlation betwixt inflation too unemployment is read the other way. (We economists seem to specialize inwards reading correlations as causal relationships, too forgetting that at that spot are ii curves that may shift inwards whatever laid of observations.) In the recession, if only the Fed could heighten inflation, the story went, it could thereby trim back unemployment. Bring on the helicopters total of money.

In whatever case, fifty-fifty the Phillips bend correlation has vanished, if it ever was there.

|

| Core inflation too unemployment. Top: fourth dimension series. Bottom: Inflation (y) vs. unemployment (x) since 2007 |

The bottom panel shows the information since 2008 as a scatterplot, amongst inflation on the left too unemployment on the bottom. Your oculus may want to describe a negatively sloped line. But actually the evidence at that spot is on the correct mitt side -- inflation dipped downwards too came dorsum upward acre unemployment stayed high. The traditional scatterplot is a chip misleading because the points are non randomly chosen, but follow each other as you lot tin ship away reckon inwards the outset plot.

The plot actually shows that at that spot is essentially no human relationship betwixt inflation too unemployment -- the line is flat. Furthermore, at that spot is a lot of vertical scatter -- the line isn't actually a line.

(A clever Fed economist in ane lawsuit parried, yes, the line is nearly flat! That's bully news. It agency if nosotros could only teach inflation upward one-half a percent nosotros would at nowadays cure unemployment. The vertical scatter emphasizes that the line is actually simply mush, non an exploitable apartment line.)

Well, in ane lawsuit again, thus much for the existent world, how does it function inwards theory? Nothing seems to a greater extent than obvious than the suggestion that if labor markets are tight, if at that spot are to a greater extent than jobs than people who desire to work, that employers volition offering higher wages, right?

No, as a thing of fact. If employers desire to attract to a greater extent than workers, they must offering higher reward relative to prices. Saying "I'll pay you lot inwards pennies'' doesn't do whatever good. Both prices too reward rising at the same fourth dimension does zippo to attract workers. If reward are "sticky'' too then the only way to have got reward rising is for production prices to autumn -- nosotros should await tight labor markets to outcome inwards less inflation inwards goods prices!

Likewise, mayhap inflation comes from tight production markets, too what could hold upward to a greater extent than natural than the thought that if at that spot is to a greater extent than demand than render that companies should heighten prices. But that also only industrial plant for relative prices.

This is ane of the first, most important, too most forgotten lessons of macroeconomics. What industrial plant for an private marketplace seat does non function for the economic scheme as a whole. The overall cost grade is a dissimilar object than (relative) prices or wages. (And, similarly, trying to heighten everyone's income yesteryear raising everyone's relative income, handing out protections to each manufacture too to labor, is every bit doomed. No, nosotros cannot delineate ourselves upward yesteryear our bootstraps.)

Now (of course) at that spot are economical theories of the Phillips curve, too practiced ones. To teach the overall grade of prices too reward to correlate amongst labor or production marketplace seat slack, you lot demand some second-order effect, some "friction.'' The easiest ane to empathise is Bob Lucas' classic theory. In this context, employers tin ship away fool people into working harder for a lilliputian acre yesteryear posting higher wages. If the people don't know that prices are going upward too, they volition think the existent wage (relative to price) is higher, too non realize they are simply beingness paid inwards devalued currency. Once they figure it out, of course, the boost to work vanishes. (Also, this is a theory of causality from unexpected inflation to higher employment, non the other way around.)

The signal hither is non that at that spot is no theory of the (apparently vanished) Phillips cure. The signal hither is that the unproblematic commonsense thought that tight markets drive inflation is wrong. If you lot desire a theory, you lot demand to become yesteryear obvious render too demand too add together some friction to pricing or to information processing, too and then you lot demand to think the Fed understands too tin ship away exploit this friction to guide us to improve outcomes than nosotros teach to on our own.

Maybe that's non how the economic scheme is wired. Maybe labor marketplace seat "tightness'' too "slack'' is non the root of inflation.

Heresy 8: Inflation Dangers

|

| Source: CBO |

- Conventional Wisdom: The danger of inflation comes if the Fed does non heighten rates chop-chop enough. Then nosotros have got a positive spiral.

- Heresy 8: The inflation danger comes from fiscal policy. Influenza A virus subtype H5N1 Greek unwind. As yesteryear low-rates too pegs evaporated due to financial problems. And too then Fed volition hold upward powerless to halt it.

Inflation, similar all crises, commonly comes from unexpected sources. Our financial province of affairs leads to a endangerment of inflation. If involvement rates rising to 5%, our authorities volition have got to pay $ 1 trillion per twelvemonth of additional debt service. It can't. This lawsuit could pile on top of a novel financial crisis too recession occasioning a few to a greater extent than trillion dollars of borrowing, on top of unreformed taxes too entitlement spending. People seeing that crisis coming volition unload authorities debt, endeavor to purchase existent things, too drive inflation. If that happens, at that spot is zippo the Fed tin ship away do almost it.

This possibility is non a forecast. It's a risk, too a modest risk, similar living higher upward an earthquake fault that breaks every few hundred years. That doesn't hateful you lot should rush out of the household correct now. But that doesn't hateful we're prophylactic either. Bond markets nevertheless trust the U.S. of A. to variety out our financial mess. But if they ever lose that faith, nosotros teach inflation -- stagflation -- that volition seem to the Fed, too to conventional wisdom, to have got come upward from nowhere.