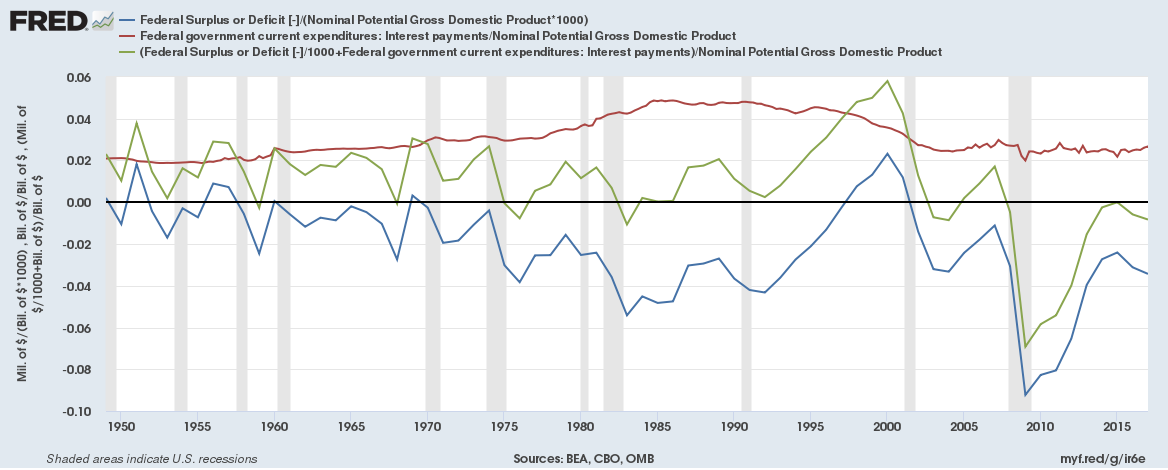

The graph is federal surplus (up) or deficit (down), non counting involvement costs, divided past times potential GDP. I made it for some other purpose, but it is interesting inward these fiscally ... interesting .. times.

Taking involvement costs out is a agency of assessing overall financial stability. If you lot pay the involvement on your credit card, the residuum won't grow over time. Granted, involvement costs are increasing -- 5% times a 100% debt/GDP ratio is a lot to a greater extent than than 5% times a 30% debt/GDP ratio, as well as involvement costs threaten to crowd out much of the ease of the budget if involvement rates larn up. But still, equally an overall mensurate of financial solvency, whether ane agency or some other you lot are paying involvement as well as and thus slow working downward debt, or if you lot are non fifty-fifty making the involvement payments as well as the residuum is growing over time, is the relevant measure.

I divided past times potential rather than actual gross domestic product thus that nosotros would focus on the deficits, as well as non run into variation induced past times GDP. If gross domestic product falls, as well as thus it makes deficit/GDP larger. The signal is to detrend as well as scale deficits past times some mensurate of our long-run mightiness to pay them. Yes, deficits after 2008 are fifty-fifty larger equally a fraction of actual rather than potential GDP. So this is the conservative choice.

Now, comments on the graph. Once you lot cyberspace out involvement costs, it is interesting how sober U.S.A. financial policy truly has been over the years. In economical expert times, nosotros run main surpluses. The impression that the U.S.A. is ever running deficits is primarily because of involvement costs. Even the notorious "Reagan deficits" were primarily payments, occasioned past times the huge spike inward involvement rates, on outstanding debt. On a revenue enhancement minus expenditure basis, non much odd was going on specially considering it was the bottom of the (then) worst recession since WWII. Only inward the extreme of 1976, 1982, as well as 2002, inward alongside steep recessions as well as inward the after illustration state of war did nosotros impact whatsoever main deficits, as well as and thus pretty swiftly returned to surpluses.

Until 2008. The terminal 10 years truly receive got been an anomaly inward U.S.A. financial policy. One may tell that the huge recession demanded huge financial stimulus, or ane may mean value $10 trillion inward debt was wasted. In either case, what nosotros simply went through was huge.

And inward the terminal information point, 2017, nosotros are sliding ane time again into territory exclusively seen inward severe recessions. That equally good is unusual.

Disclaimer: All of these measures are pretty bad. Surplus/deficit has lots of questionable reporting inward it, as well as the involvement terms exclusively has explicit coupon payments. I idea it ameliorate hither to present you lot how the easily available mutual numbers function than to larn into a large measuring exercise. I'll last doing that after for the projection that produced this graph, as well as may update.

Update: Sometimes a weblog post service makes a pocket-sized signal that tin easily last misinterpreted inward the broader context. So it is here.

The U.S.A. financial province of affairs is dire. The debt is instantly $20 trillion, larger equally a fraction of gross domestic product than whatsoever fourth dimension since the destination of WWII. Moreover, the promises our regime has made to social security, medicare, medicaid, pensions as well as other entitlement programs far exceeds whatsoever projection of revenue. Jeff Miron wrote to chide me gently for obviously implying the opposite, which is sure enough non my intent. One graph from his fantabulous "US Fiscal Imbalance Over Time":

Here, Jeff adds upwardly the promises made each twelvemonth for spending over the adjacent 75 years. Others, including Larry Kotlikoff, brand the same signal past times discounting the hereafter payments, to guess that the actual debt -- the acquaint value of what the U.S.A. owes less what it volition accept inward -- is betwixt $75 trillion as well as $200 trillion -- much to a greater extent than than the $20 trillion of actual GDP.

I've been ane of those guys wandering to a greater extent than or less alongside a sign "the debt crisis is coming" thus long that I forget to reiterate the signal on occasion, as well as Jeff rightly points out my graph taken lone could last thus misinterpreted.

In a nutshell, the work is this: The U.S.A. has accumulated a huge debt. Interest costs on that debt are already inward the hundreds of billions per year. If involvement rates rise, those costs volition ascension more. $20 trillion of debt times 5% involvement charge per unit of measurement is $1 trillion extra deficit, or fifty-fifty faster-rising debt. Unlike the illustration after WWII, when the spending was inward the past, the U.S.A. has also promised huge sum of spending inward the future.

And, equally Jeff points out, this did non starting fourth dimension inward 2008. Entitlements receive got grown as well as crowded out regular spending. Now they are growing to crowd out involvement payments. Soon they volition grow more.

Update 2

Deficits / Potential GDP; Interest costs / Potential GDP; (Deficit + involvement costs)/Potential GDP

Debt / GDP. (Thanks Vic Volpe for suggesting this ameliorate graph.)