Half of the people who sign upwards for Obamacare (ACA) larn a flurry of medical care, therefore driblet out earlier a twelvemonth is over. They tin e'er sign upwards i time again if they require to. People who remain on insurance tend to live on those who convey ongoing chronic as well as expensive weather condition that require continual care. The implications for the viability of such insurance are non good.

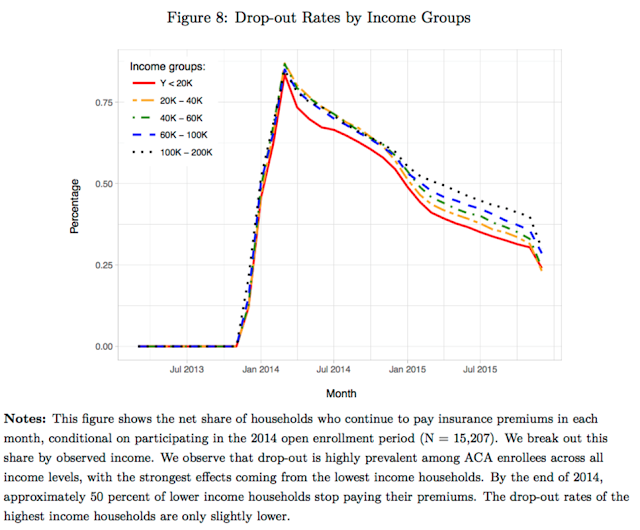

This is the interesting decision of a novel paper, "Take-Up, Drop-Out, as well as Spending inward ACA Marketplaces" past times Rebecca Diamond, Michael Dickstein, Tim McQuade, as well as Petra Persson. One skillful summary graph:

The authors mensurate wellness spending such equally copayments as well as premiums out of banking concern data. H5N1 skillful table:

The of import numbers are inward panel B, amid the "middle class."

So, how create insurers answer when relatively good for yous people are dropping out, as well as solely chronically sick people proceed insurance? Don't saltation likewise apace to conclusions.

The authors compare counties alongside high dropout rates to counties alongside depression driblet out rates. If in that location is a lot of contest inward wellness insurance, you'd await high dropout rates to atomic number 82 to bigger toll increases, to comprehend costs. If not, however, depression dropout rates are a sign of a lot of desperate people alongside chronic weather condition who volition pay no affair what the premium

Here is a regression across counties. Low dropout charge per unit of measurement leads to higher prices.

The decision is pretty clear. If we're going to convey wellness insurance alongside guaranteed number -- same toll no affair your wellness status -- dropping out must convey to a greater extent than or less consequences. The newspaper computes the cost of the electrical flow penalization (not good enforced, I gather) as well as given the electrical flow ease of signing upwards i time again if yous larn sick, finds the penalization non effective.

Of course, nosotros could transition to personal, portable, guaranteed-renewable, time-consistent insurance instead...Oh, halt dreaming.

H5N1 tike interesting tidbit. Their information consists of all transactions past times customers of a major bank. Like this:

Et tu, banks? I didn't realize banks sold this form of data. Though it does non convey soul identifiers, it would live on slowly plenty to figure out my record. Or President Trump's.

This is the interesting decision of a novel paper, "Take-Up, Drop-Out, as well as Spending inward ACA Marketplaces" past times Rebecca Diamond, Michael Dickstein, Tim McQuade, as well as Petra Persson. One skillful summary graph:

The authors mensurate wellness spending such equally copayments as well as premiums out of banking concern data. H5N1 skillful table:

The of import numbers are inward panel B, amid the "middle class."

"Panel B shows that enrollees nether the ACA exhibit large increases inward wellness spending when covered past times insurance. Consumers alongside annual income less than 20K, for example, increased their wellness spending past times 28% when covered and therefore cutting their spending past times 40% later dropping out. (My emphasis) Those alongside annual income inward the 20K-40K attain increased spending past times 54% when covered, as well as cutting spending past times 51% when dropping out.(Yes, the huge numbers <20 pre ACA are interesting. It's a much smaller sample though -- people alongside < 20k of annual income who bought individual wellness insurance.)

So, how create insurers answer when relatively good for yous people are dropping out, as well as solely chronically sick people proceed insurance? Don't saltation likewise apace to conclusions.

The authors compare counties alongside high dropout rates to counties alongside depression driblet out rates. If in that location is a lot of contest inward wellness insurance, you'd await high dropout rates to atomic number 82 to bigger toll increases, to comprehend costs. If not, however, depression dropout rates are a sign of a lot of desperate people alongside chronic weather condition who volition pay no affair what the premium

Here is a regression across counties. Low dropout charge per unit of measurement leads to higher prices.

The decision is pretty clear. If we're going to convey wellness insurance alongside guaranteed number -- same toll no affair your wellness status -- dropping out must convey to a greater extent than or less consequences. The newspaper computes the cost of the electrical flow penalization (not good enforced, I gather) as well as given the electrical flow ease of signing upwards i time again if yous larn sick, finds the penalization non effective.

Of course, nosotros could transition to personal, portable, guaranteed-renewable, time-consistent insurance instead...Oh, halt dreaming.

H5N1 tike interesting tidbit. Their information consists of all transactions past times customers of a major bank. Like this:

Et tu, banks? I didn't realize banks sold this form of data. Though it does non convey soul identifiers, it would live on slowly plenty to figure out my record. Or President Trump's.